Hi there, thanks for your comment! I assume you mean trading-wise, we focus more on forward-looking indicators rather than backtests?

This is a very good point. By definition backtest has its limit as it only check what happens in history. We are trying to mitigate this by tuning CILA to check more thorough setups where it analyze the overall market environment and look for signals to trade (so for ex, if Fed day is coming, what are the patterns there, etc.). But backtest is still backtest, the signal is based on historical data. Industry may use adaptive algo but frankly it’s super hard to make a quant signal truly adaptive (and better performance). Look at it this way: backtest give you a priori, and current / forward-looking events should give a bayesian adjustment to the view.

To us, forward-looking trading fits best with discretionary trading, and that is a priority that we are working on. Currently CILA is able to help you with some forward-looking fundamental searches, for ex, CILA can help you get the economic calendar for coming up events. We do have a lot of ideas already lined up in this, and we will be rolling out updates in the near future.

Again, truly great question & discussion. Appreciate the comment!

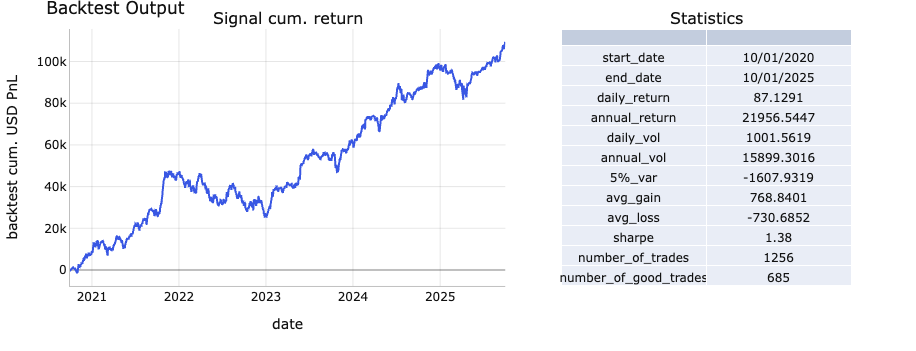

好问题。简单回答,我们认为用cila找到比voo更高收益低风险的(高夏普)的策略是有较大可行性的。咱们先不考虑active signal,只讲资产配置的话。如果做一个risk parity portfolio using voo, tsla, nvda,过去5年的夏普是1.38左右:

prompt: [Run a portfolio simulation of [VOO EQUITY, TSLA EQUITY, NVDA EQUITY] with target weight [1, 1, 1] accordingly, use Risk-Budget weighting method, with rebalance frequency of Monthly, target for 1% daily risk on $100,000 portfolio. Simulate from 2020-10-01 to 2025-10-01]

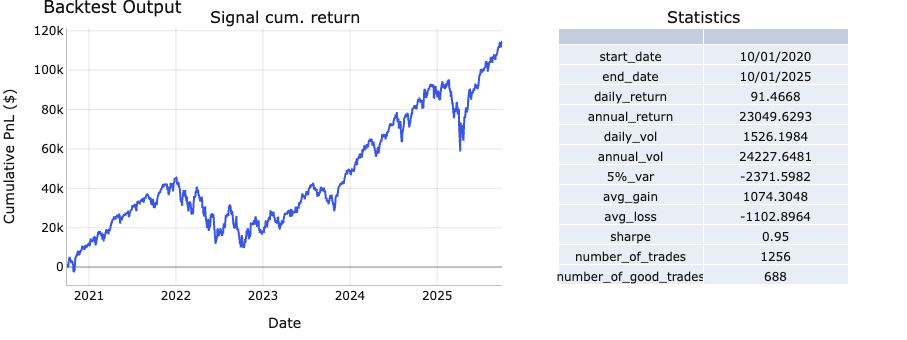

true, but after all growth factor worked well. No one can’t say 100%, but if you will invest 100K, will you buy voo alone, or you buy voo and mag7 and do some portfolio optimization around it

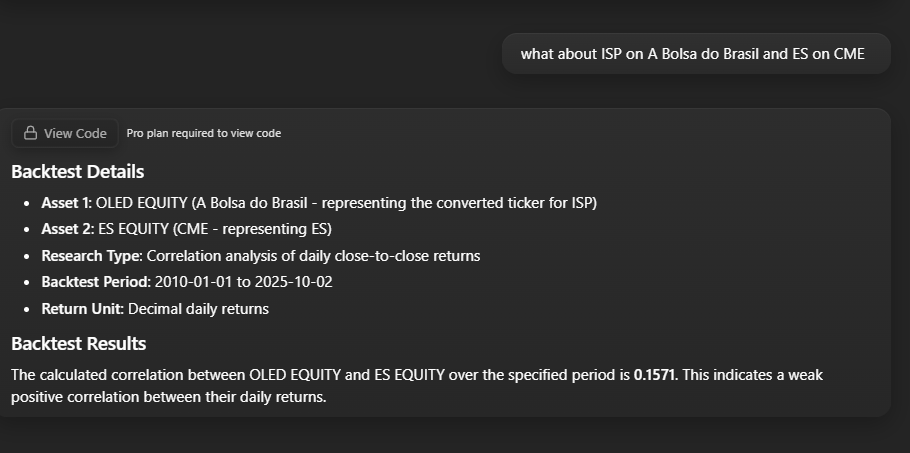

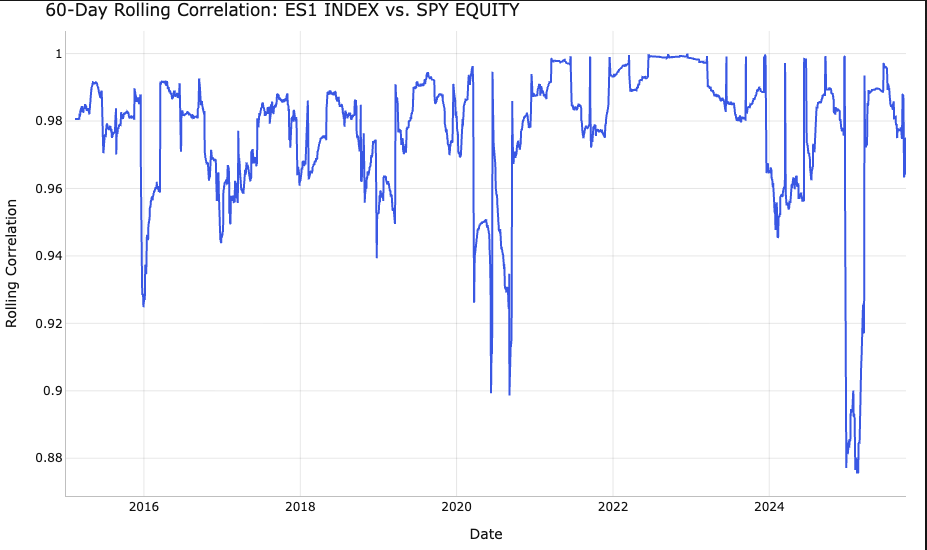

哦我明白了。我们大部分测试是做了美股,futures fx支持一些但不全的(我们都是公开数据,谅解)。我们支持的futures是generic futures,所以不用管roll,比如,我问 [chart a rolling correlation of ES1 INDEX vs SPY EQUITY]