我今天查了一下我在各大银行的信用分数,各行给出不同的分。问题:我的信用分到底是多少?

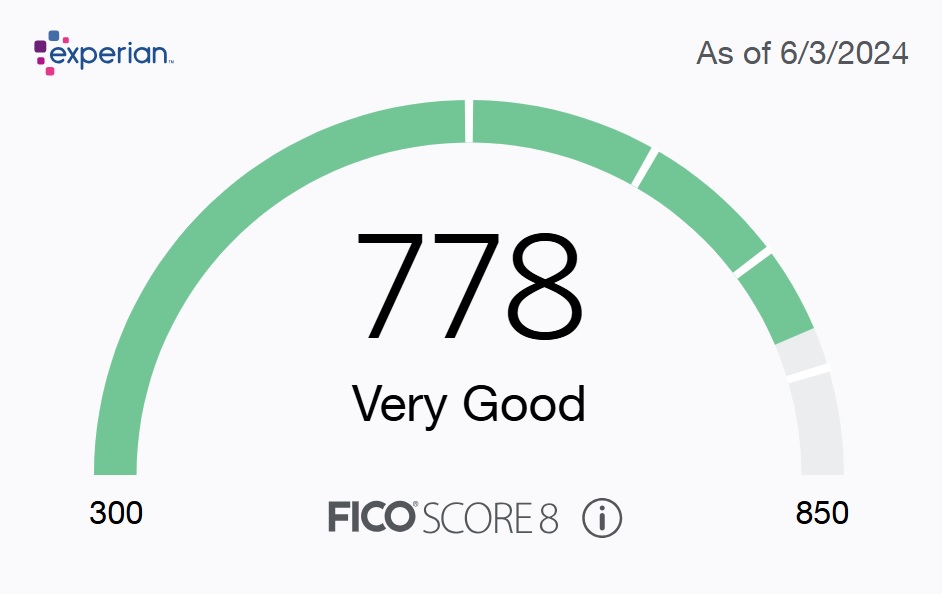

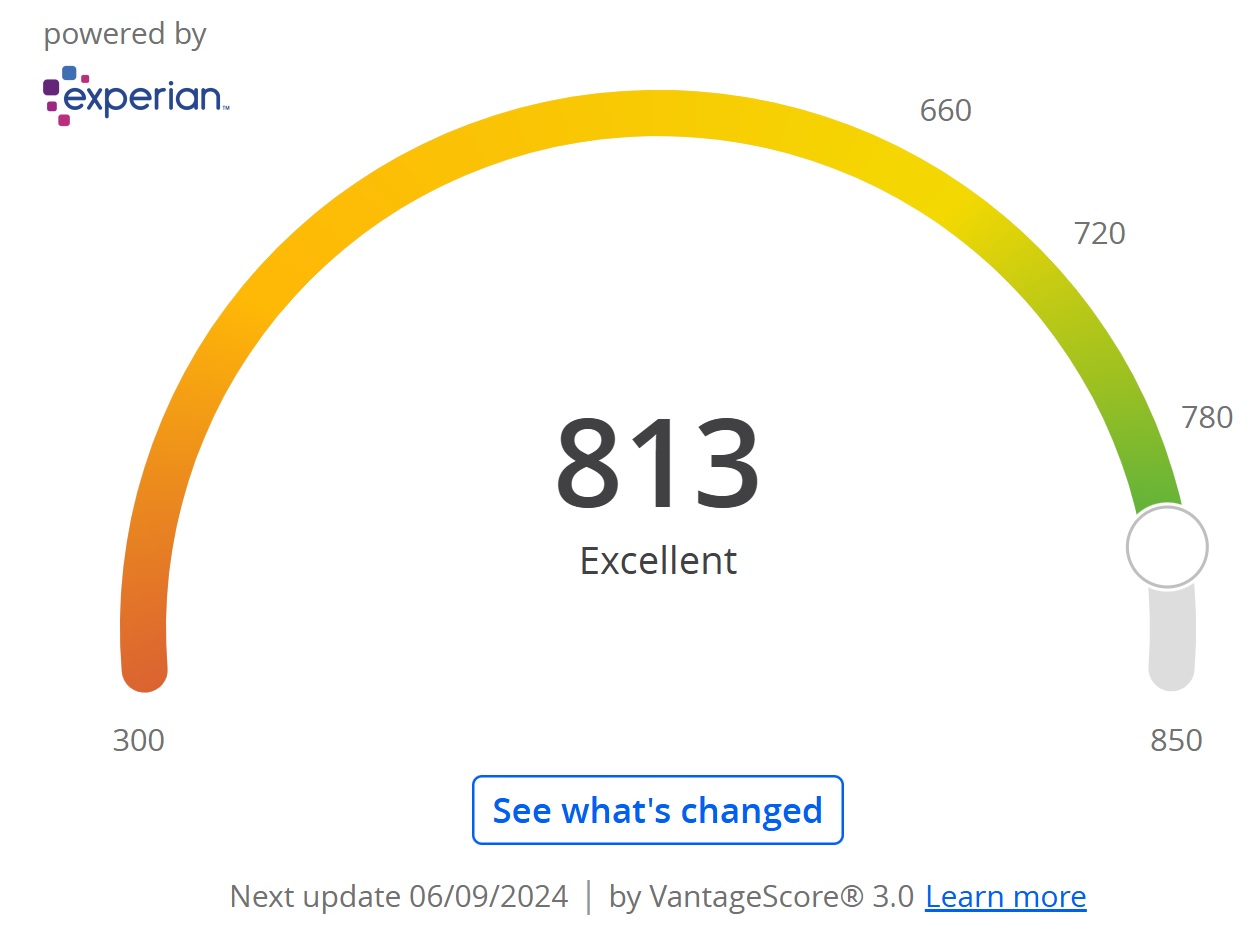

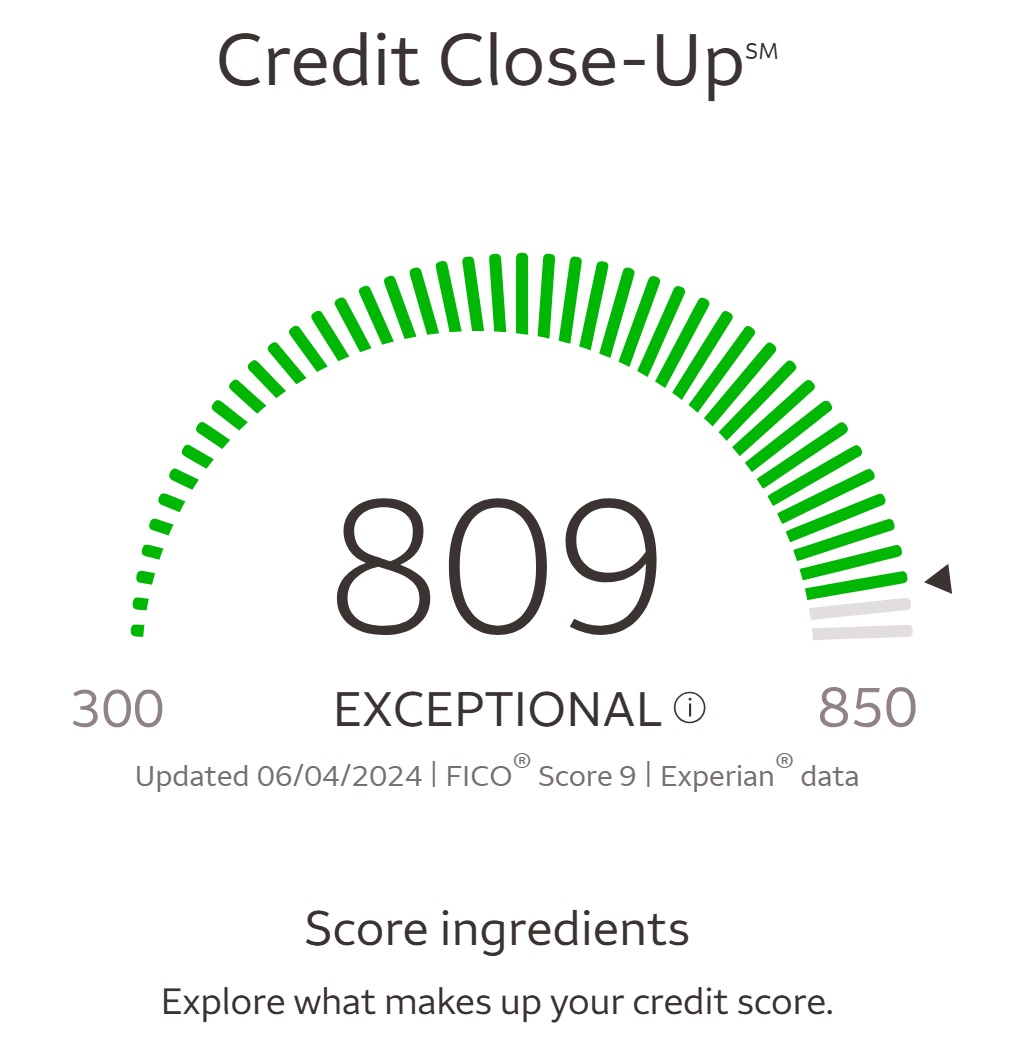

Citi:

Chase:

Wells Fargo:

Capital One:

Amex:

白金魅力时刻 ![]()

Fico 8 + experian 的data应该是最准的

咱CB的分,有啥不一样

说不一样,其实也一样

678左右吧

前排提醒注意楼主搞不好是来秀分的,不要轻易上当受骗 ![]()

我个人感觉是取最低分,那就是Amex的这个了。但奇怪的是,Citi和Amex给的分数都是基于Fico 8这个模型,但Citi给的分是一直高于800分,而Amex给的就似乎从未超过800分。

申张卡真被pull一次 收到的信里面那个最准 ![]()

见笑了,我虽然用信用卡二十多年了,但以前并没关注信用卡的相关知识,所以,"玩卡”才一年,算小白。我也不知泥潭在我发了几个贴子后迅速给了我个“白金”会员。

真不是凡尔赛。就是好奇为何每家给的信用分都不一样。

那为何Chase的FICO 8和Amex的FICO 8 有较大的差别?

我其实一直觉得这些信用分数的模型有一两个factor挺不靠谱的,如,credit utilization。一个卡给我5K的credit line,又不希望我用到30%,甚至10%的credit limit。这就不make sense。我早先的时候,以为是只要不超credit limit,用得越多越好。不然,你给我那么多credit干嘛。你银行既然给我这么多credit,当然希望我用得越多越好,只要不超过你给我的额度。在额度之内,我用得越多,而且不超额度,岂不是说明我的消费能力强,同时又对credit的把控度越好?!

刚用信用卡时,我还以为每月还全款不利于提高信用分数,毕竟,信用卡公司不能从我这儿赚钱不是。

还有,我一直认为年费卡也是scam,所以一直用的是无年费的卡。

我开始研究“玩卡”的动机来自于前几年疫情:因为有段时间在国内,长时间不用美卡,结果好多卡给我关了,我再回美时,居然陷入前几天无卡可用的尴尬,非常不方便。我就想,开几张高年费的卡,以后信用卡公司就不会给我关了吧。好天真的想法。

所以,我从去年开始,仔细地了解了一下信用卡的秘密,才意识到自己过去too young, too simple, sometimes native, 哈哈。自己的想当然的理解和信用卡公司定的客观存在的规律有较大的gap,这才开始认真了解信用卡的人为规定的各种规矩,并修改自己的认知和行为。

Chase写的不是vantage score?

有道理!反正不能想当然。得好好了解现实的情况,不能自己想当然。

推荐阅读:Reverse Engineering FICO 8. The FICO algorithm is proprietary and… | by Michael Fowlie | Medium

泥潭白金用户分数不应该这么高 ![]()

谢谢推荐,文章看完了。FICO algorithm居然像可口可乐的配方一样,还保密呢。老美真是一招鲜,吃遍天哈。文章作者还得reverse enginerring来figure out这个算法。

Perfect profiles look like this:

计划未来两年多多申请卡拿sub,拉下FICO 8分,追上泥潭平均水平。

原来C1还有这个外号了 ![]()

![]()

![]()

![]()

打个比方,你完成了一套体操/跳水动作,台下的几个裁判的打分大概率也不完全一样。这几个信用局就是给你打分的裁判。

我最近申请过的C1 Savor one, 把我给拒了。我还试图pre-qualify for C1的卡(想来张C1 VX),结果C1说我不qualify for他们的任何卡。

有意思的是,我大约六七年前拿过C1的一张卡,具体哪张我忘记了,但是是一张无年费的。疫情期间我一段时间没用它,也没关注,C1给我的卡给关了,感觉C1是渣行!