TLDR

Contribution 可以随时取出, 会收到 1099-R, codeJ, 不用交税. 但需要报税. 详细见楼下讨论.

2023 年, 朋友听我的话, 存了$6500 cash进 Roth IRA

CASH CONTRIBUTION CURRENT YEAR (Cash)

+$6,469.60

Feb-28-2023

CASH CONTRIBUTION CURRENT YEAR (Cash)

+$30.40

后来他反悔了, 又取出来.

Jan-22-2024

EARLY DIST NO EXCEPT CASH (Cash)

-$6,500.00

交了6500, 取出6500,应该完全不收税的吧. 但他被fidelity系统认为是 early distribution需要收税.

-

Contribution 不用交税的资料索引

-

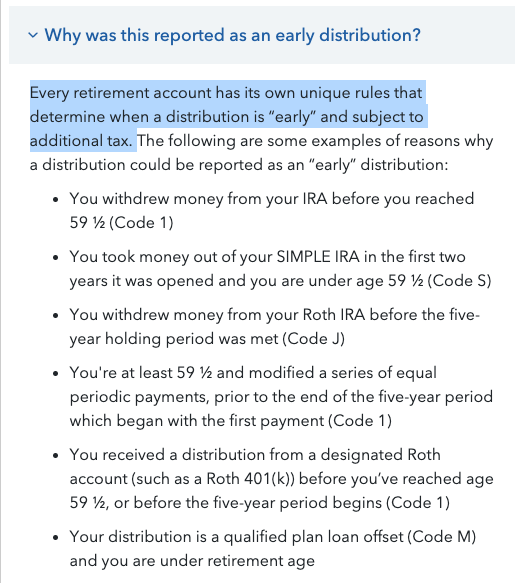

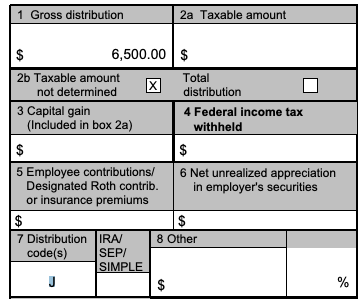

收到的 1099-R 上面对这部分是 code J

Code J 是这个意思 You withdrew money from your Roth IRA before the five-year holding period was met (Code J)

问了 GPT, 也认为这个税收错了, 所以坛友们认为是 Fidelity 系统出错了? 除了联系Fidelity之外没有别的办法? 按说取钱就是应该从contribution 开始取呀, 这种低级错误不该犯吧.

GPT 回答:

It seems like you’re facing an issue where Fidelity is categorizing your withdrawal as an “early distribution” rather than a simple return of your Roth IRA contributions. Let me break down the situation and offer some insights:

Key Details:

- Contributions: You made two contributions to your Roth IRA:

- $6,469.60 on Feb 28, 2023.

- $30.40 on Feb 28, 2023.

- Withdrawal: On Jan 22, 2024, you withdrew $6,500.

Why Fidelity Might Think It’s an Early Distribution:

- Roth IRA Withdrawal Rules:

Roth IRA withdrawals are generally taken in the following order: - Contributions (tax- and penalty-free)

- Conversion amounts (if applicable, subject to different rules)

- Earnings (taxable and potentially penalized if withdrawn early)Since the total of your two contributions adds up to $6,500, you should indeed be able to withdraw this amount without any tax or penalty because it’s part of your contributions.

- Fidelity’s System:

The key issue could be a technicality in how Fidelity’s withdrawal system tracks contributions versus earnings. Even though you withdrew exactly your contributions, Fidelity might be treating it as a “distribution” without proper recognition that these were just contributions. Sometimes, the system defaults to categorizing early withdrawals as taxable or penalized, especially if the Roth IRA isn’t yet meeting the required holding period for qualified distributions. - Incorrect Code on 1099-R:

The 1099-R form generated by Fidelity might have incorrectly categorized the withdrawal under the early distribution code, which typically happens when the system is unsure of the timing and type of withdrawal. In this case, the form might have issued a “Code J” or another code for early distributions that doesn’t meet Roth IRA qualified distribution criteria, even though it should be categorized as a non-taxable, non-penalized return of contributions. - Timing Confusion:

Even though you contributed in 2023, your withdrawal in January 2024 could still be processed as an early distribution if there’s a mismatch in how Fidelity is interpreting the account’s timeline or if they are mistakenly applying rules based on the 5-year holding period rule, which is separate from the rule for withdrawing contributions.

What You Should Do:

- Verify Contribution vs. Earnings:

Double-check your Roth IRA account with Fidelity. If the $6,500 is entirely your contribution and there are no earnings in the amount, make sure the system recognizes it as such. - Contact Fidelity:

Reach out to Fidelity customer service. Explain that you withdrew only contributions, and ask them to correct the distribution code on your 1099-R. They may need to adjust the withdrawal details to avoid categorizing it as an “early distribution.” It may be a simple system error. - Check Your 1099-R:

If you already received a 1099-R, ensure it accurately reflects the withdrawal. If they issued a code that’s incorrect, ask them to send a corrected form with the proper classification (which should reflect a return of contributions rather than an early distribution). - Tax Filing:

If the form isn’t corrected and you need to file your taxes, you may need to manually adjust for the correct withdrawal type. As long as the withdrawal was from your contributions, it should not be taxed or penalized, regardless of the distribution code.

Summary:

Fidelity might be incorrectly processing the withdrawal as an early distribution due to a system or coding issue, even though you withdrew your contributions. You’ll need to contact Fidelity to clarify the withdrawal and potentially correct the distribution code. If this is not resolved in time for tax filing, make sure to adjust your tax return accordingly to reflect that it was a return of contributions, not earnings.