首先,利益相关:AMZN投资者,赔钱中所以预测有很大不确定

第二,非投资建议,错误希望有懂行的朋友指正。

第三,亚马逊最主要的估值来自于AWS,其他业务的数据没有具体核对,用了卖方预测。

作为在AMZN身上反复亏钱的人,财报前做了AMZN的功课,但实际上就是错了。

. 1.此预测主要有下面两个假设

- Amazon invest in Anthropic/OAI 现金流如下:

| Item | Amount | What It Means |

|---|---|---|

| $50B FCF burn | $50B | Amazon’s massive capex cycle (AI infrastructure, data centers, logistics) is expected to consume most/all of its free cash flow. In 2025A, FCF was only $11.2B — down from $35.5B in 2024 — because capex is surging. This $50B represents cumulative FCF shortfall over the next 2-3 years as capex outpaces operating cash flow. |

| $50B OpenAI | $50B | Not literally investing in OpenAI — this refers to the competitive spending required to match OpenAI/Microsoft’s AI investment. Microsoft has committed ~$80B+ to AI infrastructure. Amazon/AWS must spend at a similar scale to remain competitive in foundation models and cloud AI services. |

| $15–25B Anthropic | $15–25B | Direct investment in Anthropic (Claude’s maker). Amazon has already committed up to $8B. The thesis is that Anthropic needs significantly more capital to compete at the frontier, and Amazon should fund it — both as a strategic investment and to keep AWS as the primary cloud provider for Anthropic’s training/inference. |

| $40–50B+ to run an $800B rev biz | $40–50B | Baseline working capital and maintenance capex to operate a ~$800B revenue business. This includes inventory, fulfillment infrastructure, delivery fleet, existing cloud capacity, etc. This IS the net working capital / maintenance component you asked about. |

| Less $100B cash | ($100B) | Amazon’s cash + marketable securities on hand (~$100B as of 2025). This is the offset against the total need. |

- Additional $200 Capex,2026E实际上可能更多

** 2. 卖方观点预计:**

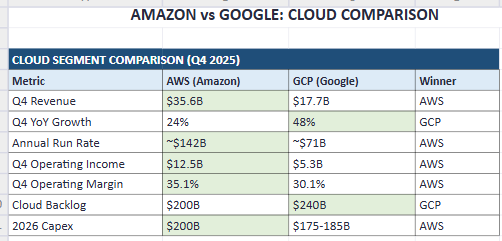

AWS对比其他Hyperscalers:

| Company | Cloud Growth (YoY) | Key Context |

|---|---|---|

| Google (GCP) | +48% | Fastest growth among the giants; accelerating significantly. |

| Microsoft (Azure) | +39% | Stronger growth than AWS, driven heavily by AI demand. |

| Amazon (AWS) | +24% | Lowest percentage growth of the three. While revenue beat estimates ($35.6B vs $34.9B expected), it significantly trails peers in momentum. |

2. 2026 CapEx Spending “Arms Race”

The primary shock in the thread (e.g., “$200B CapEx”) is Amazon’s massive spending forecast for 2026, which dwarfs its peers.

- Amazon: ~$200 Billion (Projected). This is the “massive number” mentioned in the chat. It focuses on AI chips (Trainium), data centers, and satellites.

- Google: $175 – $185 Billion (Projected). Second highest spender, nearly doubling its previous year’s spend.

- Microsoft: ~$150 Billion (Estimated). Based on current run rates of ~$37.5B/quarter.

- Meta: $115 – $135 Billion (Projected). Focuses heavily on AI infrastructure for social platforms rather than public cloud sales.

3. Main Points of Comparison

- Spending vs. Growth Mismatch: The core negativity in the thread comes from the fact that Amazon is planning to spend the most money ($200B) while delivering the slowest cloud growth (24% vs. Google’s 48%).

- Profit Margins: AWS margins were reported around 35%, which is healthy, but the “EBIT guide miss” mentioned in the chat suggests the massive spending is eating into overall profitability faster than investors like.

- Investor Sentiment: While Google and Microsoft are seeing their spending rewarded with massive growth spikes (39-48%), Amazon’s “catch-up” spending is being viewed with skepticism, leading to the “ramen and fireball” comments about stock losses.

4. 个人计算,

主要都是AI推导的,SOTP我就不贴出来