Even if you meet these requirements, you can’t exclude days of presence in 2021 as a teacher or trainee if you were exempt as a teacher, trainee, or student for any part of 2 of the 6 prior calendar years. But see the Exception below.

(后面特定例外略)

Pub. 519, p5:

You will not be an exempt individual as a teacher or trainee in 2021 if you were exempt as a teacher, trainee, or student for any part of 2 of the 6 preceding calendar years. However, …

(后面特定例外略)

我构建了一个特殊情景,会出现比较好玩的结果:

第 1 年,不在美国

NRA

第 2 年,首次 F / J 签证在美,之前年份在美日期从没豁免 SPT 计算过,因此本年豁免

NRA

Except as provided in paragraph 2 of Article 8, paragraph 2 of Article 17, and Articles 18, 19, 20, 22, 23, 24 and 26 of this Agreement, the United States may tax its residents

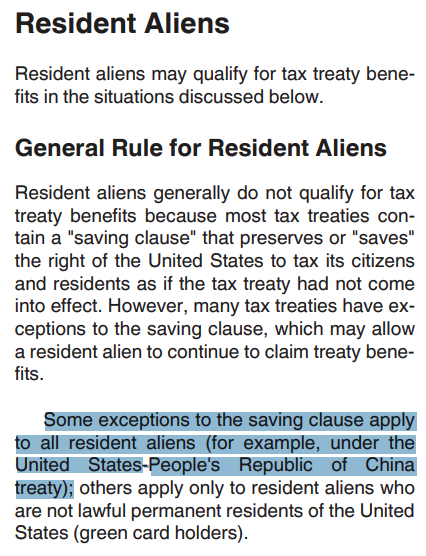

这个文档其实本来是给 VITA 志愿者的简明参考手册,相当精要总结了各国学生学者享受的 treaty 差异,后面也列出了一些国家的特例。

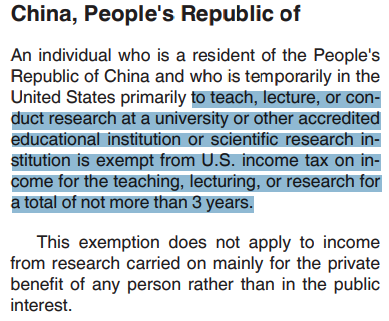

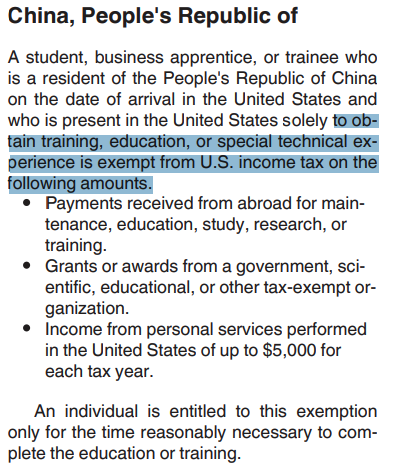

中国的特例在 p10,用一段话把 J-1 和 F-1 的情况都包括了:

China Treaty Articles 19, 20(c)

…

The U.S. treaty with China provides that a scholar is exempt from tax on earned income for 3 years. After 2 years, a scholar will become a resident alien for tax purposes but is still entitled to 1 more year of tax benefits under the treaty. The treaty also provides that students have an exemption of up to $5,000 per year for income earned while they are studying or training. In most cases, the student will become a resident for federal tax purposes in their sixth calendar year. Students from China can continue to claim the treaty benefits on their resident alien tax return (if they still meet the definition of a student).

其实 Pub. 519 也提了这事,只是太冗长了比较难找到 (p47)。

而且使用了 “saving clause” “exception” 之类难以理解的法律术语、也没有单独指出来中美 treaty 是有这个 exception 的。

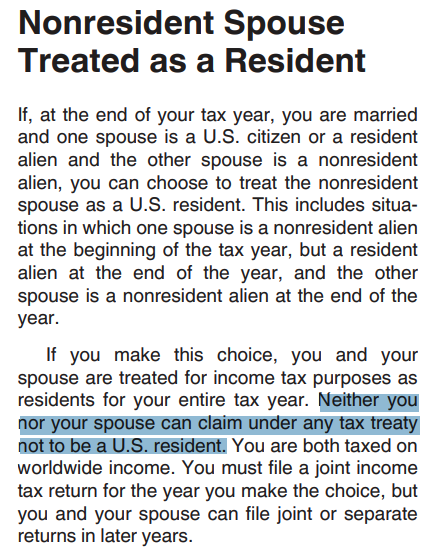

也特别指出了 NRA + RA 视为 RA 适用:

Students, Apprentices, Trainees, Teachers, Professors, and Researchers Who Became Resident Aliens

Generally, you must be a nonresident alien stu-dent, apprentice, trainee, teacher, professor, or researcher in order to claim a tax treaty exemp-tion for remittances from abroad for study and maintenance in the United States, for scholar-ship, fellowship, and research grants, and for wages or other personal service compensation. Once you become a resident alien, you can generally no longer claim a tax treaty exemption for this income. However, if you entered the United States as a nonresident alien, but you are now a resident alien for U.S. tax purposes, the treaty exemption will continue to apply if the tax treaty’s saving clause (explained earlier) provides an exception for it and you otherwise meet the re-quirements for the treaty exemption (including any time limit for claiming treaty exemptions, explained below). This is true even if you are a nonresident alien electing to file a joint return, as explained in chapter 1.

…

Notwithstanding any provision of the Agreement, the United States may tax its citizens. Except as provided in paragraph 2 of Article 8, paragraph 2 of Article 17, and Articles 18, 19, 20, 22, 23, 24 and 26 of this Agreement, the United States may tax its residents (as determined under Article 4).

This article is excepted from the “saving clause” of paragraph 2 of the Protocol, so its benefits are available to persons who otherwise qualify even if they become U.S. residents.

这报个税感觉比搞科研都累…

这报个税感觉比搞科研都累… )

)