前几天看了篇论文 https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2741701

文中的观点大概是当IV低的时候买带杠杆的大盘指数,当IV高的时候去杠杆买Treasury。以移动平均钱来作为IV高低的临界点。

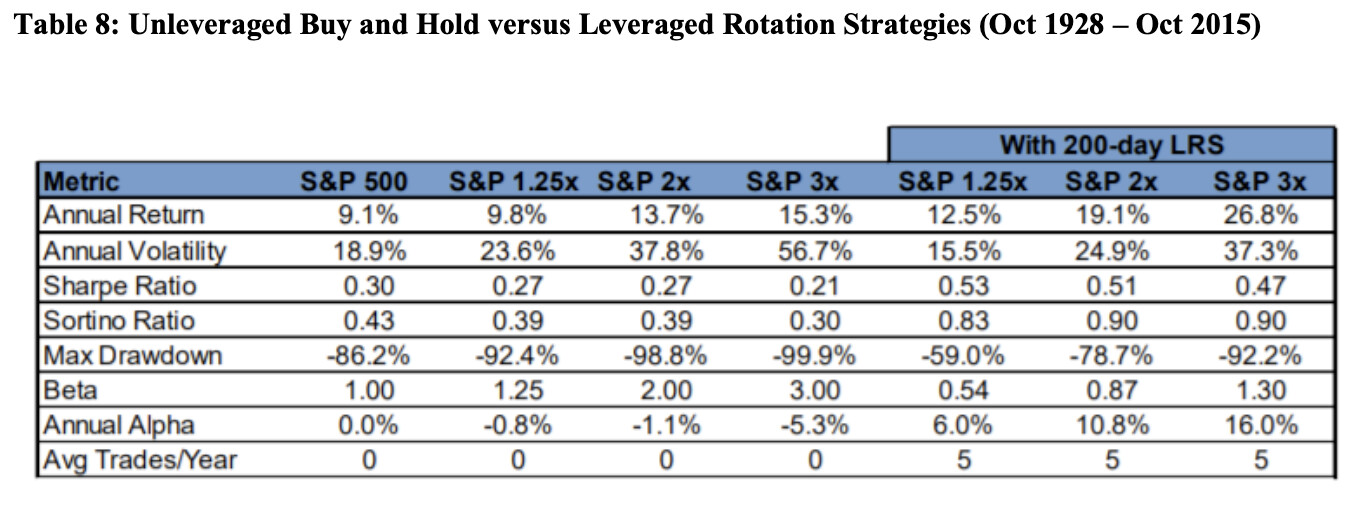

With this knowledge, our systematic Leverage Rotation Strategy (“LRS”) is as follows:

When the S&P 500 Index closes above its Moving Average, rotate into the S&P 500 and use leverage to magnify returns.

When the S&P 500 Index closes below its Moving Average, rotate into Treasury bills to manage risk.

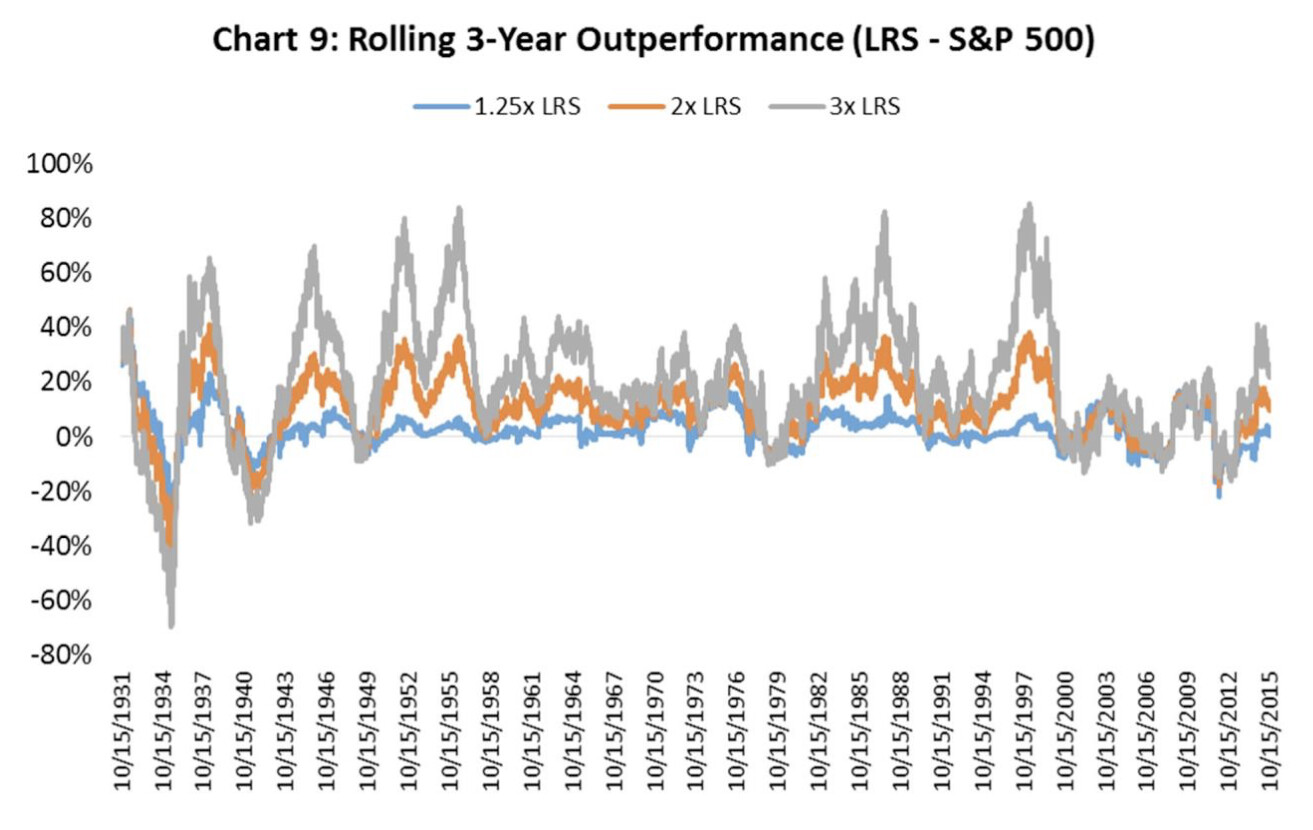

从回测数据里用200日EMA移动平均线的话效果非常好,在没有增加volatility的情况下提升了年化收益。

这篇文章有一点很吸引我:之前讨论过的UPRO/TMF的策略默认只适用于低利率环境,在1980年之前的高利率时代是很惨的,但是这个策略似乎在接近100年的跨度了一直对大盘保持优势。

缺点也不是没有,因为一旦跌破200均线就要全部移仓,可能会导致很大的税问题,感觉比较适合tax-free account。

之前看过物理粉讲杠杆投资的文章,抛砖引玉一下,不知道大家对这篇文章的理念有什么想法?

25 个赞

感觉好像和UPRO/TMF risk parity 的道理是类似的,risk parity 的话也是股票的volatility高的时期比例就小。你说的这个策略则是只考虑了股票那边的IV没管债券这边,基本把债券当作安全资产了。

4 个赞

是的 而且债券这边是没有上杠杆的 但我很惊讶在升息环境下这个策略还没崩

4 个赞

不加杠杆的债券就算跌出翔其实也崩不了吧 和股票崩盘相比还算是安全了

4 个赞

话说感兴趣的话可以回测一下今年的情况这个策略表现如何。用均线的话如果只看当前价格和200日的交叉 会让交易特别频繁;如果是50日均线和200日均线的交叉 则会相当滞后 可能像今年3月这种急速下跌根本避不开… 反正均线这东西比较玄学

2 个赞

简单算了下 今年要调仓两次 2.27 杠杆ETF换TLT 5.27 TLT换杠杆ETF

3倍杠杆 YOE 44.5% 最大回撤 -47%

2倍杠杆 YOE 34.5% 最大回撤 -23%

今年你track的那几个策略回撤怎么样

4 个赞

可以看我的雪球组合: 雪球-聪明的投资者都在这里

你这个只需要调仓两次的 具体是什么和200日均线的交叉?

1 个赞

哦哦 这种操作的话2020年不是问题 问题在于比如说2015年的一段时间 SPY来回穿200日均线 就得不停地买入卖出

1 个赞

hmm 这个动态调整的策略似乎没有直接40/60或者45/55得表现好 有意思

2 个赞

Yep, 今年形势变化太快,比如3月份还是大跌 股市volatility巨高,4.1 rebalance的时候就把股市比例调低了,但是4月整个是个巨夸张的大涨,这样动态调整就错过了一波好机会…

3 个赞

请教一下杠杆怎么上?Stock 杠杆可以用TQQQ,Bond带杠杆用什么呢?感觉券商的融资部分利息挺贵的

3 个赞

Risk Parity and 60/40 are dead now…FED kills it.

1 个赞

其实只有高通胀会 低利率(只要还是正的)和无限QE并不会 参考2009-2016那段时期

但现在的预期是美国会面临高通胀(以及如何计算),只是不知道何时而已。

3 个赞

通胀预期可以在这里看:

目前正在相当艰难的突破2%,这是美联储的目标,一旦高于2%很快美联储政策就会变的让它回去。现在这个时代,通胀持续低迷是自然趋势,想让通胀变高反而不容易…

2 个赞

刚才看了下数据,2020整体来说UPRO/TMF是跑赢大盘的 但是如果从3月份开始看的话是一直跑输大盘的 优点是2、3月的时候跌的少

不知道今年会是什么结果,再看吧

1 个赞